Writing Regression Routines in R

Goals for the talk

This talk is is about writing linear regression routines in R and how they fit together

I'll cover intuition and implementations

- Ordinary least squares (OLS)

- Ridge Regression

- Generalized Linear Models

- Elastic Net

Implementations are meant to be short and readable

Anti-Goals

I'm not going to:

- spend a lot of time on statistical properties

- talk about optimality characteristics

- show code that's been optimized for speed

Why should we care about linear models?

They are old (Gauss 1795, Legendre 1805).

Random Forests (RF) are at least as simple and often do better at prediction.

Deep Learning (DL) dominates vision, speech, voice recognition, etc.

LM vs Rf

LM generally has lower computational complexity

LM is optimal RF is not

LM can outperform RF for certain learning tasks

RF is more sensitive to correlated noise

LM vs DL

See most arguments for LM vs RF

We understand characteristics of the space we are in with LM. Not so with DL.

RESULT: We know how things go wrong with LM, not with DL.

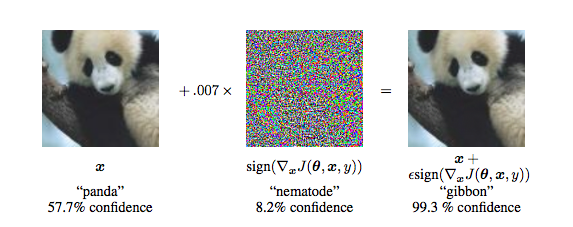

Breaking DL with Adversarial noise

Figure from Explaining and Harnessing Adversarial Examples by Goodfellow et al.

Advantages of LM

Computationally Efficient

LM is not simply a prediction tool - results are interpretable

Diagnostics for assessing fit and model assumptions

LM is compatible with other models

> train_inds = sample(1:150, 130)

> iris_train = iris[train_inds,]

> iris_test = iris[setdiff(1:150, train_inds),]

> lm_fit = lm(Sepal.Length ~ Sepal.Width+Petal.Length,

+ data=iris_train)

> sd(predict(lm_fit, iris_test) - iris_test$Sepal.Length)

[1] 0.3879703

> library(randomForest)

> iris_train$residual = lm_fit$residuals

> iris_train$fitted_values = lm_fit$fitted.values

> rf_fit = randomForest(

+ residual ~ Sepal.Width+Petal.Length+fitted_values,

+ data=iris_train)

>

> lm_pred = predict(lm_fit, iris_test)

> iris_test$fitted_values = lm_pred

> sd(predict(rf_fit, iris_test)+lm_pred -

+ iris_test$Sepal.Length)

[1] 0.3458326

> rf_fit2 = randomForest(

+ Sepal.Length ~ Sepal.Width+Petal.Length,

+ data=iris_train)

> sd(predict(rf_fit2, iris_test) - iris_test$Sepal.Length)

[1] 0.40927The not so ordinary least squares model

Assume

Find

Derivation

What if X isn't full rank?

my_lm = function(X, y) {

XTy = crossprod(X, y)

XTX = crossprod(X)

QR_XTX = qr(XTX)

keep_vars = QR_XTX$pivot[1:QR_XTX$rank]

solve(XTX[keep_vars, keep_vars]) %*%

XTy[keep_vars]

}

What if X is "almost" not full rank?

Numerical Stability

> x1 = 1:100 > x2 = x1 * 1.01 + rnorm(100, 0, sd=7e-6) > X = cbind(x1, x2) > y = x1 + x2 > > qr.solve(t(X) %*% X) %*% t(X) %*% y Error in qr.solve(t(X) %*% X) : singular matrix 'a' in solve > > beta = qr.solve(t(X) %*% X, tol=0) %*% t(X) %*% y > beta [,1] x1 0.9869174 x2 1.0170043 > sd(y - X %*% beta) [1] 0.1187066 > > sd(lm(y ~ x1 + x2 -1)$residuals) [1] 9.546656e-15

Should I include x1 and x2 if they are colinear?

> X = matrix(x1, ncol=1) > beta = solve(t(X) %*% X, tol=0) %*% t(X) %*% y > beta [,1] [1,] 2.01 > sd(y - X %*% beta) [1] 6.896263e-06

Dropping Unbiasedness

We can sometimes get better prediction if we allow some bias (Cramér-Rao bound).

Add a parameter α to control bias.

Can be solved with

my_ridge = function(X, y, lambda) {

XTy = crossprod(X, y)

XTX = crossprod(X)

QR_XTX = qr(XTX)

keep_vars = QR_XTX$pivot[1:QR_XTX$rank]

solve(XTX[keep_vars, keep_vars] +

lambda*diag(length(keep_vars)) %*%

XTy[keep_vars]

}

Adding model selection

We can select which regressors do a good job predicting the dependent variable by adding another constraint

The Ridge Part

The Least Absolute Shrinkage and Selection Operator (LASSO) Part

my_lmnet = function(X, y, lambda, alpha, maxit=10000, tol=1e-7) { beta = beta_old = rep(0, ncol(X)) quad_loss = Inf

for(j in 1:maxit) {

quad_loss_old = quad_loss

beta = coordinate_descent(X, y, lambda, alpha, beta_old)

quad_loss = quadratic_loss(X, y, lambda, alpha, beta)

if(quad_loss > quad_loss_old) break

beta = beta_old } list(beta=beta_old, iterations=j) }

coordinate_descent = function(X, y, lambda, alpha, beta_old,

W=rep(1,nrow(X)) {

beta = beta_old

for (l in 1:length(beta)) {

beta[l] = soft_thresh(sum(W*X[,l]*(y - X[,-l] %*% beta_old[-l])),

sum(W)*lambda*alpha)

}

beta / (colSums(W*X^2) + lambda*(1-alpha))

}

soft_thresh = function(x, g) {

x = as.vector(x)

x[abs(x) < g] = 0

x[x > 0] = x[x > 0] - g

x[x < 0] = x[x < 0] + g

x

}

quadratic_loss = function(X, y, lambda, alpha, beta, W=1) {

-1/2/nrow(X) * sum(W*(z - X %*% beta)^2) +

lambda * (1-alpha) * sum(beta^2)/2 + alpha * sum(abs(beta))

}

how do we get from lmnet to glmnet?

A little bit about the glm

- g is the link function

- Element of W are inversly proportional to variance of response which depend on slope coefficients

- See Bryan's notes for more explanation

my_glm = function(X, y, family=binomial, maxit=25, tol=1e-08) {

beta = rep(0,ncol(A))

for(j in 1:maxit) {

eta = X %*% beta

g = family()$linkinv(eta)

gprime = family()$mu.eta(eta)

z = eta + (y - g) / gprime

W = as.vector(gprime^2 / family()$variance(g))

beta_old = beta

beta = solve(crossprod(X,W*X), crossprod(X,W*z),

tol=2*.Machine$double.eps)

if(sqrt(crossprod(beta-beta_old)) < tol) break

}

list(beta=beta, iterations=j)

}

IRLS

Now back to glmnet

my_glmnet = function(X, y, family=binomial, maxit=25, tol=1e-08) {

beta = rep(0,ncol(X))

for(j in 1:maxit) {

eta = X %*% beta

g = family()$linkinv(eta)

gprime = family()$mu.eta(eta)

z = eta + (y - g) / gprime

W = as.vector(gprime^2 / family()$variance(g))

beta_outer_old = beta

quad_loss = Inf

for(k in 1:maxit) {

beta_inner_old = beta

quad_loss_old = quad_loss

beta = coordinate_descent(X, z, lambda, alpha, beta_old, W)

quad_loss = quadratic_loss(X, z, lambda, alpha, beta, W)

if(quad_loss > quad_loss_old) break

beta = beta_inner_old

}

if(sqrt(crossprod(beta_inner_old-beta_outer_old)) < tol) break

}

list(beta=beta_inner_old)

}

Wrapping up

Currently working on an out-of-core version ioregression.

I'll talk about making this fast at RFinance.

Thanks to Bryan Lewis for the GLM notes.

Thanks to AT&T Labs Research (Taylor Arnold and Simon Urbanek) for helping to make this happen.